Jun 7, 2017 Report: Divestment of Pensions Could Cost Trillions

New report finds fossil fuel divestment would cost the nation’s top 11 pension funds up to $4.9 trillion over the long term

WASHINGTON, D.C. (JUNE 7, 2017) – A first of its kind study finds public pension funds could lose trillions of dollars if they divested from fossil fuel related investments.

The new report, authored by Prof. Daniel Fischel of the University of Chicago Law School, together with coauthors Christopher Fiore and Todd Kendall of the economic consulting firm Compass Lexecon, analyzes 11 of the nation’s top pension funds—including the largest state pension fund, the California Public Employees’ Retirement System (CalPERS) as well as municipal funds in New York City, Chicago and San Francisco – to determine the financial impact of divesting from fossil fuel securities. The results indicate that these funds would lose up to a combined $4.9 trillion over 50 years due to reduced portfolio diversification.

“Our report shows divestment would cost pension funds trillions of dollars, an outcome that likely would significantly harm returns for pensioners,” stated Prof. Fischel. “Given the unique role of the energy sector in the economy, investors who chose to remove traditional energy from their investments reduce the diversification of their portfolios and thereby suffer reduced returns and greater risk. And that’s not all. These costs are further compounded when considering the additional costs of transactional fees, commissions, and compliance costs that are unavoidable when divesting. Divestment may seem noble, but it has real financial implications for pension funds, many of which are already struggling to provide reliable investment returns to beneficiaries.”

In order to accurately calculate the cost of divesting, Prof. Fischel and his coauthors used all available data on the current holdings of each fund to estimate the returns on the same or similar holdings over the past 50 years. These returns were compared to returns over that same period from an otherwise identical risk-adjusted portfolio, stripped of stocks targeted by divestment advocates. The report considers lost diversification benefits due to divestment from coal, oil and natural gas companies, as well as broader divestment including utility companies, which creates a range of possible outcomes.

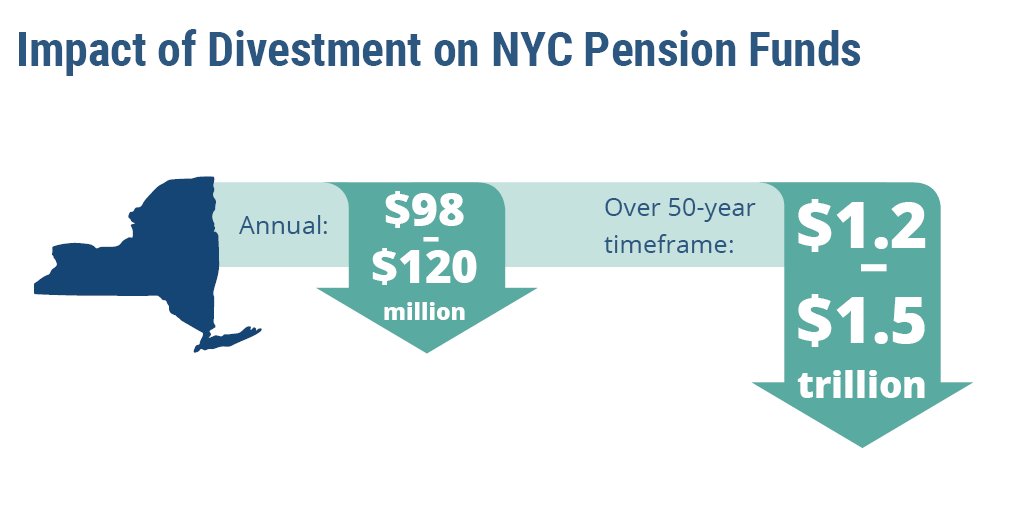

The report finds that a divestment policy would hit California’s CalPERS fund the hardest, with reductions in returns ranging from $2.3 to $3.1 trillion over 50 years, and up to $290 million annually. New York follows close behind, with the New York City Employee Retirement System (NYCERS) — the largest municipal public employee retirement system in the United States – estimated to suffer between $502 and $692 billion in lower returns over 50 years. The annual impact for NYCERS ranges between $41 and nearly $60 million.

These impacts are merely the tip of the iceberg for many public pensions that are already deeply underfunded. Currently, the 100 largest public pensions in the U.S. are funded below 70 percent, and total unfunded liabilities are approximately $1.25 trillion. Further reductions in investment returns could exacerbate the issue and lead to financial consequences for pensioners or taxpayers in the future.

“At a time when pensions across the country are struggling to generate sufficient returns, divestment would impose a staggering financial penalty, making it even more difficult to meet payout obligations for their beneficiaries while having no impact on the environment,” said Jeff Eshelman, senior vice president for operations and public affairs at the Independent Petroleum Association of America (IPAA). “As a consequence of these mounting costs, pensions would either have to cut payments or seek other funding sources to make up the shortfall. That would put an even heavier burden on taxpayers who could be responsible for financial bailouts to compensate for these losses.”

The newly released report analyzes the following funds: CalPERS, the San Francisco Employee’s Retirement System, the New York City Teacher’s Retirement System, New York City Police Pension Fund, New York City Fire Department Pension Fund, New York City Employee Retirement System (NYCERS), New York City Board of Education Retirement System, the Chicago Policemen’s Annuity & Benefit Fund, Laborers’ and Retirement Board Employees’ Annuity and Benefit Fund of Chicago, Firemen’s Annuity and Benefit Fund of Chicago, and the Municipal Employees’ Annuity and Benefit Fund of Chicago.

Read the full report and fact sheet online.

Additional Background

The report is an ongoing part of the Divestment Facts program, launched by IPAA in 2015 to provide data-driven research and facts on the ineffectiveness of fossil fuel divestment. This new report represents the fifth installment in a series of recent studies that have sought to quantify the true costs of the #DivestmentPenalty. The first study, also authored by Prof. Fischel, found that divested equity portfolios would incur an annual loss of 50 basis points on a risk-adjusted basis over a 50-year period, representing a 23 percent reduction in returns relative to a diversified portfolio. The second report, authored by Prof. Bradford Cornell of Caltech, quantified the impact of divestment on Harvard, Yale, MIT, NYU, and Columbia, with divestment-related losses for those institutions ranging up to $107.8 million per year. The third report and fourth report, authored by Prof. Bessembinder of Arizona State University’s Carey School of business, found that transaction costs and other frictional costs associated with divestment could rob an endowment by as much as 12 percent of its value over a 20-year timeframe. Prof. Bessembinder goes on to find that the average endowment “hole” created by divestment results in a 15.2 percent drop in transfers from endowment accounts to school programs. That means increases in annual tuition rates (or a reduction in existing scholarships) of as much as $3,265 per student per year or as much as an 11.5 percent reduction in faculty spending, which in turn could lead to fewer classes or increased class sizes.

Universities and Pensions Agree:

- Vermont Pension Investment Committee Report: “In our opinion, other portfolio-wide potentially material financial risks and opportunities posed by climate change are not addressed by fossil fuel divestment. Divestment does not: address climate change material risks (including technological, policy, physical) evident in other industries from agriculture and forestry to infrastructure, buildings and insurance. Divestment does not provide enhanced exposure to companies involved in energy efficiency and renewable energy. Publicly held equity divestment only transfers ownership of fossil fuel securities; it cannot provide fossil fuel alternatives with any new financial resources.” LINK

- New York State Comptroller Thomas DiNapoli: “My fiduciary duty requires me to focus on the long-term value of the Fund. To achieve that objective the Fund works to maximize returns and minimize risks. Key to accomplishing this objective is diversifying the Fund’s investments across sectors and asset classes – including the energy sector, where fossil fuels continue to play an integral role in powering the world’s electricity generators, industry, transportation and infrastructure.” LINK

- California Public Employees’ Retirement System (CalPERS) CEO Anne Stausboll: “Engagement is the first call of action and is the most effective form of communicating concerns with the companies in which we invest. That is why, when it comes to climate change and its risks, Calpers’ view is that the path to change lies in engaging energy companies, instead of divesting them. If we sell our shares then we lose our ability as shareowners to influence companies to act responsibly.” LINK

- CalPERS: “The Board and Staff also have a fiduciary responsibility under the California Constitution to ‘diversify the investments of the system so as to minimize the risk of loss and to maximize the rate of return, unless under the circumstances it is clearly not prudent to do so’ …These fiduciary obligations generally preclude CalPERS from sacrificing investment performance for the purpose of achieving goals that do not directly relate to CalPERS operations or benefits.” LINK

- CalPERS, California State Controller Betty Yee: “We are fiduciaries of this fund. And our sole focus is and must continue to be how we are going to pay the benefits to our public sector workers and our educators who have earned these benefits during their work life.”

- The CEO of the Hispanic Chambers of Commerce of San Francisco: “Taxpayers will have to pick up for the tab to meet promised pensions that the investments don’t cover. Additional pension-fund shortfalls that divestment would cause are precisely what businesses owners don’t need.” LINK

Biography of Professor Fischel

Professor Daniel R. Fischel is the president of the economic consulting firm Compass Lexecon and the Lee and Brena Freeman Professor of Law and Business Emeritus at The University of Chicago Law School. The previous Dean of The University of Chicago Law School, Prof. Fischel has published over 50 articles in leading legal and economics journals, many of which have been cited by courts at all levels including the Supreme Court, and has authored two books on economics and corporate law. He is a former professor at Northwestern University Law School and was a Supreme Court clerk for Justice Potter Stewart.

The study, Fossil Fuel Divestment and Pension Funds, was commissioned and financed by the Independent Petroleum Association of America (IPAA). The views expressed by way of this paper are those of Professor Fischel and his coauthors; they do not speak for affiliated universities or IPAA. Read more about Professor Fischel here.

About the Independent Petroleum Association of America

The Independent Petroleum Association of America (IPAA) is a national upstream trade association representing thousands of independent oil and natural gas producers and service companies across the United States. Independent producers develop 90 percent of the nation’s oil and natural gas wells. These companies account for 54 percent of America’s oil production, 85 percent of its natural gas production, and support over 2.1 million American jobs. Learn more about IPAA by visiting www.ipaa.org and following @IPAAaccess on Twitter.